苏ICP备112451047180号-6

“营改增”对出版业公司的财务影响及对策研究

摘要: 税收是国家收入重要的来源 ,它的本质在于对社会资源的重新分配。税收涉及的方面也颇多,从公司到行业到社会,这其中几乎都离不开税收。因此,对于税收的改革,社会各层次也给予了高度关注。我国税制改革的时间具体来说是1994年,根据国际上的经验,初步建立了标准化的生产型增值税,这一做法严格区分了营业税和增值税的征税范围。从此以后,营业税和增值税如同两条平行线,不会相互干涉与交错。这在促进国家经济的发展和改善社会的福利等方面都有了较为深远的影响。随着人民生活水平的提高和经济的快速增长,我国也经历了产业模式的重大转型,第三产业受到了越来越多的关注与发展。但是两税并行的情况造成了对第三产业的重复征税,从一定程度上约束了第三产业的进步。因此,“营改增”成为了我国促进产业转型,推动经济增长的必然措施。

截止到2016年5月1号,我国已经全面实行了“营改增”,营业税自此退从此淡出了人们的视线。出版业作为第三产业中的潜力产业和21世纪的“朝阳产业”,在整个行业税制改革的中,“营改增”是其重要的方向。本文选取了出版业中最具典型和代表的公司—中南传媒为案例,从税负、资产负债表、利润表和现金流量表这四个角度对其“营改增”的概况进行阐述,并且针对“营改增” 出现的影响,提出自己的建议。

关键词: “营改增” 出版业公司 财务影响

VAT financial impact on publishing enterprises on the strategy research and analysis

Abstract: Taxation is an important source of national income, and its essence lies in theredistribution of social resources. Tax involves a lot of aspects, from the company to the industry to the community, which is almost no tax revenue. Therefore, for the tax reform, social levels have also given a high degree of concern. China's tax reform time is specific in 1994, according to international experience, the initial establishment of a standardized production-based value-added tax, this approach strictly distinguish between the business tax and value-added tax taxation. Since then, business tax and value-added tax as two parallel lines, do not interfere with each other, not staggered. This has played a very important role in promoting the development of the national economy and improving the welfare of the society. With the continuous development of the national economy, China has also undergone a major transformation of the industrial model, the tertiary industry has been more and more attention and development. But the business tax and value-added tax in parallel to the secondary industry caused by the repeated taxation of the tertiary industry, to a certain extent, bound the development of the tertiary industry. Therefore, the "camp by" has become China's industrial development, promote national economic growth inevitable measures.

As of May 1, 2016, China has fully implemented the "VAT", since the business tax from the fade out of people's attention. Publishing industry as the potential industry in the tertiary industry and the 21st century "sunrise industry", in the entire industry tax reform, "VAT" is its important direction. This paper chooses the most typical and representative company in the publishing industry - Zhongnan Media as a case, from the tax burden, balance sheet, income statement and cash flow table of these four angles of its "VAT" to elaborate, and For the "VAT" the impact of the emergence of their own recommendations.

Key words:VAT Publishing company Financial impact

目录

引言 1

第1章“营改增”相关概念 2

1.1 相关概念 2

1.1.1 营业税的概念 2

1.1.2 增值税的概念 2

1.1.3 营业税与增值税的比较 3

1.2 “营改增”的必要性 3

第2章“营改增”对出版业公司影响的一般性分析 6

2.1出版业公司概述与财务特点 6

2.1.1 出版业公司概述 6

2.1.2 出版业公司的财务特点 6

2.2“营改增”对出版业公司的财务影响 7

2.2.1 对税负的影响 8

2.2.2 对资产负债表的影响 8

2.2.3 对利润表的影响 8

2.2.4对现金流量表的影响 9

第3章 案例分析——以中南传媒为例 10

3.1中南传媒的概况 10

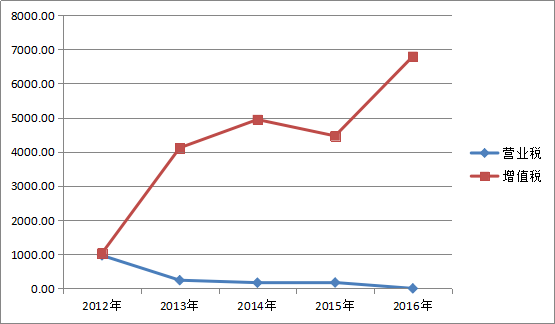

3.2“营改增”对中南传媒税负的影响分析 10

3.3 “营改增”对中南传媒资产负债表的影响分析 11

3.4“营改增”对中南传媒利润表的影响分析 13

3.5 “营改增”对中南传媒现金流量表的影响分析 14

第4章 出版业公司应对“营改增”的建议 16

4.1合理选择公司的供应商 16

4.2做好税务申报的工作 16

4.3优化税务筹划方案 16

4.4加强公司的财务管理 16

结术语 18

参考文献 19

致谢 21

引 言

随着我国经济的不断发展,人们对于文化的需求也在增长。在这样的背景下,出版业不断发展。然而长期以来,营业税和增值税并行、对纳税人多次征税的状况一直约束着第三产业的成长。由于出版业属于第三产业,是营业税主要的征收对象,这在某种程度上加深了出版业的税收负担。随着2012年的“营改增”的推进,第三产业成为这个税制改革的主要受益者。截止2016年5月1日,我国“营改增”已经全面实施。作为“营改增”进程的参与者和受益者,出版业能够更加直观地表现出其对于公司的财务影响。

因此,本文从出版业公司入手,以中南传媒为例,从营业税与增值税相关的概念出发,通过参阅大量研究材料和分析各种数据,从税负、资产负债和利润等几个层面具体分析“营改增” 给中南传媒带来的财务影响,并据此提出自己的建议。

参考文献

【1】潘文轩,公司“营改增”税负不减反增现象分析[J].商业研究,2013(01):145-150

【2】许善达.吃好“营改增”的大蛋糕[J].中外管理, 2012(12):92-93

【3】李萍.“营改增”将在经济改革中发挥更大牵引作用[N].中国税务报,2014,03-07(A01)

【4】财政部财政科学研究所、新闻出版总署财务司联合课题组,艾立民等. 完善我国支持新闻出版业发展的财税政策建议[J].经济研究参,2013(26):40-51

【5】曹芳.我国文化产业税收政策探析[D].西南财经大学,2014

【6】施文泼、贾康. 我国增值税“扩围”改革的必要性[J]. 经济研究参考,2011(12):19

【7】郭焕英.“营改增”会计处理及其对公司财务影响解析[J]. 商场现代化,2016(22):123-125

【8】张曦彤.“营改增”后企业会计处理的变化研究[J]. 商业经济,2017(03):81-83.

【9】季树芬. 增值税抵扣视角看“营改增”对服务业的影响[J]. 时代金融,2017(02):25-27.

【10】吕连菊, 邱茹芸. 浅析“营改增”对公司财务管理的影响[J].会计之友,2015(16):89-91

【11】韩悦. 浅析“营改增”对现代服务业的影响及应对[J]. 知识经济,2017(02):41-42.

【12】赵连伟. “营改增”的企业成长效应研究[J]. 中央财经大学学报,2015(07):20-27

【13】费飞.浅谈“营改增”对现代服务业会计核算的影响[J]. 当代会计,2017(01):30-31

【14】刘成杰,张甲鹏. “营改增”对国内就业影响的再认识[J]. 税务研究,2015(06):66-71.

【15】陈斌.“营改增”全面实施后对出版行业的影响[J].财经界,2016(11):319

【16】Simon James.The Importance of Fairness in Tax Policy:Behavioral Economics and the UK Experience[J].International Journal of Applied Behavioral Economics,2014(31)

【17】Iris Claus.Is the value added tax a useful macroeconomic stabilization instrument?[J].Economic Modelling,2013(30)

【18】Petr David,Pavel Semerád.Possibilities of Measuring Tax Evasion Related to Fuel Sale[J].Procedia Economics and Finance,2014(12)

【19】Christian Hubert Ebeke.Dointernation Alremittance Saffect the Level And the Volatility of Over Nment Tax Revenues?[J].J.Int.Dev.,2014,267

【20】Mukheijee.T.A survey of Corporate Leasing Anaysis[J].Financial Management, 1991(20):96-107

【21】Graham Bannoek.Reforming value added tax.Institute of economic affairs[J].2001(6)

【22】Emran.MS,Stiglitz.JE,On selective Indirect Tax Reform in Developing Countries[J]Journal of Public Economics,2005,89(4):599-623

【23】Carbonnier.C,Who Pays Sales Taxes? Evidence from French VAT Reforms,1987—1999 [J]Journal of Public Economics,2007,91(5-6):1219-1229